Home Childcare Providers (RSGE)

![]()

We are proud to insure you as a home childcare provider (RSGE) affiliated with the FSSS (CSN), and to make this hub of information available to you! It includes all the details about your group insurance plan.

To be eligible for the group insurance plan, you must be recognized as a permanent home childcare provider by the Ministère de la Famille and care for three or more children in your home daycare.

Once you meet these two criteria, you are eligible three months after you have received Ministère de la Famille recognition.

You must sign up for group insurance once you are recognized as eligible.

You must fill out the enrolment form and return it to us within 30 days following the date you become eligible.

You must fill out the enrolment form and return it to us within 30 days following the date you become eligible.

Attach a "void" cheque to your form.

Send your enrolment form and "void" cheque to us in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec (Québec) G1V 4H6

When your application is submitted to us within the 30 days following your eligibility date: your application for insurance is accepted as of your eligibility date.

When your application is submitted to us more than 30 days after your eligibility date: your application for insurance is accepted on the first day of the 14-day premium payment period that coincides with or follows the date on which Beneva received your application. Some of your selections may be subject to evidence of insurability.

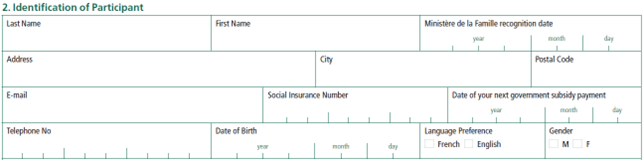

- Confirm that you are recognized by the Ministère de la Famille.

-

Specify all elements that allow us to identify you.

-

Also indicate the date on which you were recognized by the Ministère de la Famille and the date on which your next government contribution is paid.

-

Then identify your coordinating office and specify your employment situation.

-

Identify your spouse (if applicable).

-

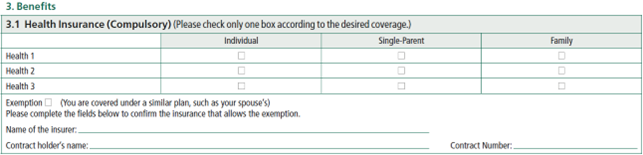

Make your health insurance coverage selection.

-

As needed, see “Your plan at a glance” in the Documentation section to find out more about each level of coverage.

-

If you want to opt out, make sure you provide all of the information requested.

- Specify your choice of status for dental care.

- Please note:

- Individual status is assigned automatically.

- You must check “I wish to opt out of this coverage” if you don’t want to sign up for this benefit.

- Select your short term disability insurance coverage.

- Please note:

- Option 1 ($300) is assigned automatically and at the time you enrol, the four options available are offered to you without evidence of insurability.

- Subsequently, any request to increase this coverage is subject to evidence of insurability.

- You can subscribe to long term disability insurance without providing evidence of insurability.

- Please note:

- If you sign up for this benefit, the option is assigned as the same as for short term disability insurance.

- Subsequently, any request to add this coverage is subject to evidence of insurability.

- For Participant’s Basic Life Insurance and Participant’s AD&D Insurance, you can select Option 1 ($25,000) or Option 2 ($50,000) without providing evidence of insurability.

- Please note:

- Option 1 ($25,000) is assigned automatically.

- You must check “I wish to opt out of this coverage” if you don’t want to sign up for this benefit.

- Subsequently, any request to add or increase this coverage is subject to evidence of insurability.

- You can apply to enrol in Participant’s Optional Life Insurance.

- Please note:

- This coverage is always subject to evidence of insurability.

- You must first sign up for Participant’s Basic Life. Insurance plus Participant’s AD&D Insurance Option 2 ($50,000).

- You can subscribe to Spouse’s and Dependent Children’s Life Insurance without evidence of insurability.

- Please note:

- This benefit is granted automatically.

- You must check “I wish to opt out of this coverage” if you don’t want to sign up for this benefit.

- Subsequently, any request to add this coverage is subject to evidence of insurability.

-

You can apply to enrol in Spouse’s Optional Life Insurance.

- Please note:

- This coverage is always subject to evidence of insurability.

- You must first sign up for Participant’s Basic Life. Insurance plus Participant’s AD&D Insurance Option 2 ($50,000).

-

If you subscribe to life insurance for yourself, you must designate a beneficiary.

-

Three steps:

1. Choose either your estate or a designated beneficiary.

2. If you are naming a beneficiary, specify your relationships with that beneficiary.

3. Specify whether the beneficiary is revocable or irrevocable.

-

If you want to sign up for the optional life insurance for yourself or your spouse and you are a non-smoker, you must declare this information in order to receive a lower premium.

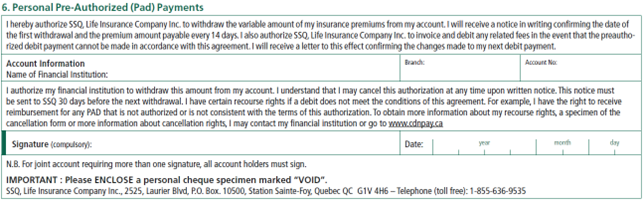

- Premiums are paid by means of preauthorized debit payments.

- You must:

- Provide your bank account details.

- Provide a cheque marked "void".

-

Then, sign the enrolment form and send it to us along with your "void" cheque.

-

Send your enrolment form and "void" cheque to us in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

The following benefits are compulsory:

- Health 1 – Individual status (subject to an exemption entitlement)

- Short term disability insurance

If no choice is made, the benefits below are granted automatically:

- Health 1 – Individual status

- Dental Care – Individual status

- Short term disability insurance – Option 1 ($300)

- Participant’s Basic Life Insurance + Participant’s AD&D Insurance – Option 1 ($25,000)

- Spouse’s and Dependent Children’s Basic Life Insurance

Enrolment in the benefits below is subject to a minimum participation period of 36 months:

- Health 2

- Health 3

- Dental Care

- The only payment method accepted is preauthorized debit.

- The debit is taken every 14 days on the day your government contribution is paid.

- Your 14-day premium periods start on the day of your debit.

- If we are unable to take the debit for your premium for two consecutive premium periods:

- your certificate will be terminated

AND - a letter of non-payment will be sent to the Régie de l’assurance maladie du Québec (RAMQ)

- your certificate will be terminated

Description :

Several benefits are offered depending on the coverage level you choose (Health 1, Health 2 or Health 3), giving you access to the health care and services that meet your needs:

- Prescription drugs:

- Health 1: RAMQ list + $5.00 deductible per prescription drug purchase + 67% reimbursement

- Health 2: Regular list + $5.00 deductible per prescription drug purchase + 75% reimbursement

- Health 3: Regular list + $5.00 deductible per prescription drug purchase + 80% reimbursement

- Travel Insurance

- Other Medical Expenses

- Health Care Professionals

- Vision Care

- This benefit is compulsory, subject to the exemption entitlement.

- The available coverage statuses are:

- Individual

- Single-parent

- Family

- IMPORTANT: Note that Quebec’s Act respecting prescription drug insurance requires people who are insured by a private health insurance plan to cover their spouse and dependent children if they are not already covered by another private health insurance plan.

- You must select one of the coverage levels: See the “Your plan at a glance” brochure to learn the coverage offered at each level.

- Health 1

- Health 21

- Health 31

1 If you select Health 2 or Health 3 coverage, you must maintain your participation for at least 36 months before you can request to decrease your coverage level.

Description:

An excellent complement to health insurance, dental care insurance adds several benefits to your group insurance, including:

- Basic Dental Care

- Restorative Dental Care

- This benefit is optional, but with automatic enrolment.

- The benefit is automatically granted with Individual status unless otherwise indicated on the enrolment form.

- The available coverage statuses are:

- Individual

- Single-parent

- Family

- If you choose this benefit, you must maintain your participation for at least 36 months before you can request to decrease your coverage level.

Description :

This benefit is automatically included in your contract. In the event of personal issues that may affect your normal functioning or that of one of your dependents, support, consultation, counselling and intervention services are available through the Assistance Program. Coverage is limited to 9 hours of services per calendar year for all insured members of the same family.

Description :

In the event of disability, this coverage provides you with weekly benefits during your first year of disability.

- This benefit is compulsory.

- Benefits start: After 7 days of disability

- Benefits end: After 52 weeks of disability or at age 65

- You must choose one of the following four options:

- Option 1 ($300 per week, non-taxable)

- Option 2 ($400 per week, non-taxable)

- Option 3 ($500 per week, non-taxable)

- Option 4 ($600 per week, non-taxable)

Description:

In the event of long term disability, this coverage provides you with monthly benefits subsequent to the short term benefits which end after 52 weeks of disability or at age 65.

- This benefit is optional.

- Benefits start: After 52 weeks of disability

- Benefits end: At age 65.

- If you opt to enrol, your level of benefits (Option 1, 2, 3 or 4) will be the same as with the short term disability insurance.

- Option 1 ($1,300 per month, non-taxable)

- Option 2 ($1.650 per month, non-taxable)

- Option 3 ($2,000 per month, non-taxable)

- Option 4 ($2,350 per month, non-taxable)

- This benefit is available without evidence of insurability when you submit your enrolment form within 30 days following the date you are eligible for group insurance.

- Any request to add or increase this benefit beyond the 30 days following the date you are eligible will require evidence of insurability.

Description:

The two benefits described below are inseparable.

Participant’s Life Insurance

In the event of your death, this option provides the beneficiary you designated with $25,000 or $50,000.

Participant’s Accidental Death and Dismemberment (AD&D) Insurance

In case of accidental death or accidental loss of a limb, you or your designated beneficiary will receive a certain percentage of the amount of $25,000 or $50,000 you chose, without exceeding 100%.

- This benefit is optional, but with automatic enrolment.

Coverage Option 1 ($25,000) is granted automatically unless otherwise indicated on your enrolment form. - You must choose a coverage level:

- Option 1 ($25,000)

- Option 2 ($50,000)

- All the options are available without evidence of insurability when you submit your enrolment form within 30 days following the date you are eligible for group insurance.

- Any request to add or increase this benefit beyond the 30 days following the date you are eligible will require evidence of insurability.

Description:

This option allows you to add between $10,000 and $200,000 to the Participant’s Basic Life Insurance coverage.

- This benefit is optional.

- You can choose from 1 to 20 units of $10,000.

- To enrol, you must first sign up for Participant’s Basic Life Insurance and AD&D Insurance Option 2 ($50,000).

- Any request to add or increase this benefit is subject to evidence of insurability.

Description:

This option allows you to receive an amount of $5,000 subsequent to the death of a dependent.

However, this amount is $10,000 in the event of the death of a child if you have no spouse at the time the death occurs.

- This benefit is optional, but with automatic enrolment. This benefit is granted automatically unless otherwise indicated on your enrolment form, regardless of the health insurance coverage status you select.

- This benefit is available without evidence of insurability when you submit your enrolment form within 30 days following the date you are eligible for group insurance.

- Any request to add this coverage beyond the 30 days following the date you are eligible will require evidence of insurability.

Description:

This option allows you to add between $10,000 and $100,000 to the Spouse’s Basic Life Insurance coverage.

- This benefit is optional.

- You can choose from 1 to 10 units of $10,000.

- To enrol, you must first sign up for Participant’s Basic Life Insurance and AD&D Insurance Option 2 ($50,000).

- Any request to add or increase this benefit is subject to evidence of insurability.

Need to make a claim?

Four ways to choose from.

Online

Submit your claim with your Client Centre and get reimbursed in 48 hours for most benefits.

The mobile app

Download the free Beneva mobile application and get reimbursed in 48 hours for most benefits.

Application mobile disponible sur l'Apple App Store

Application mobile disponible sur l'Apple App Store  Application mobile disponible sur le Google Play Store

Application mobile disponible sur le Google Play Store

By mail

Send us the claim form along with the original receipts. Personalized forms are available in Client Centre. Simply fill them out, print and sign.

You can't find the form you're looking for on the list? Call our Client Service.

1 888 651-8181

With the insurance card

Present your insurance card at the dentist's office or at the pharmacy. You will pay only for the expenses not covered under your group insurance contract.

IMPORTANT: All health insurance claims must be received by us no later than 12 months after the date the expenses were incurred. After that, they will not be reimbursed.

Want to know whether the medical expenses you incurred are eligible for reimbursement?

The Expenses Covered feature lets you go to a specific benefit to see the applicable terms of reimbursement.

Easily access this information by clicking on the shortcut Check covered medical expenses or Check covered dental care expenses on the Client Centre homepage.

Your insurance booklet provides detailed information on your coverage.

IMPORTANT: All health insurance claims must be received by us no later than 12 months after the date the expenses were incurred. After that, they will not be reimbursed.

The easiest way to have your drugs reimbursed is to show your insurance card to your pharmacist.

The pharmacist can submit the claim to us directly and charge you only your deductible and coinsurance.

For any other situation involving a drug claim, please see Section 8 of your booklet – How to submit claims.

IMPORTANT: All health insurance claims must be received by us no later than 12 months after the date the expenses were incurred. After that, they will not be reimbursed.

TRAVEL INSURANCE AND ASSISTANCE

In the event of an emergency that occurs while the insured is out of their home province, all travel assistance services and most eligible travel insurance expenses are handled by our travel assistance service, as long as the insured contacts them.

However, if you have a claim to submit after you come home (you have 12 months to do so), or you want to check your travel insurance coverage before you go, call us at one of the following numbers:

Canada and the United States: 1 800 465-2928

Elsewhere in the world, collect: 514 286-8412

TRIP CANCELLATION INSURANCE

When making a claim, the insured must provide us with supporting documentation as quickly as possible. We will refuse any claim that is submitted more than 12 months after the date on which the expenses were incurred.

For any questions about your travel insurance, please see the brochure on that subject: Travel insurance brochure.

Many health insurance expenses can be claimed online through the Client Centre. You can also make a claim using the Beneva Mobile Services app.

It’s also possible to mail in a claim by submitting the appropriate form. A personalized version is available in the Client Centre and at beneva.ca. The bills must be paid, with the originals attached to the claim.

IMPORTANT: All health insurance claims must be received by us no later than 12 months after the date the expenses were incurred. After that, they will not be reimbursed.

You can present your insurance card to your dentist and pay the portion of expenses not covered by us.

IMPORTANT: For all expenses covered by Dental Care insurance, claims must be received by us no later than 12 months after the date the expenses were incurred. After that, they will not be reimbursed.

The assistance program puts you in touch with qualified providers who are ready to help you.

All assistance program providers belong to recognized professional orders (nurses, occupational therapists, psychologists, social workers, counsellors, etc.), ensuring that you get high-quality, confidential service. To speak with a professional, call the assistance program at 1 877 480-2240. Have your contract number on hand.

The disability insurance claim must be submitted to us no later than 90 days following the start of total disability.

To do this, you must fill out both disability claim forms (Statement of insured AND Statement of attending physician), available in the Documentation section, and submit them to us.

Note: These two forms must be submitted together.

For further information, please see the question > I recently started disability leave. What should I do to receive my benefits?

The life insurance benefit claim form is available by contacting us directly.

The claim and proof of death must be submitted to us within 90 days following the date of death.

Eligible events:

- Marriage/civil union

- Cohabitation for a period of one year

- Birth/adoption/custody of a child

- Termination of spousal coverage

- Separation/divorce

- Death of a dependent

When your request is submitted to us within 30 days following the event: Your request is accepted as of the date of the event.

When your request is submitted to us more than 30 days following the event: Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva received your request.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible events:

- Marriage/civil union

- Cohabitation for a period of one year

- Birth/adoption/custody of a child

- Termination of spousal coverage

- Separation/divorce

- Death of a dependent

When your request is submitted to us within 30 days following the event: Your request is accepted as of the date of the event.

When your request is submitted to us more than 30 days following the event: Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva received your request.

Please note:

- The increase in health coverage is accepted even if the 36-month minimum participation period is not over.

- A new 36-month minimum participation period starts on the date the change request is approved if you choose Health 2 or Health 3.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible events:

- Marriage/civil union

- Cohabitation for a period of one year

- Birth/adoption/custody of a child

- Termination of spousal coverage

- Separation/divorce

- Death of a dependent

When your request is submitted to us within 30 days following the event: Your request is accepted as of the date of the event.

When your request is submitted to us more than 30 days following the event: If your 36-month minimum participation period is over, your request is accepted on the first day of the premium payment period that coincides with or follows the date Beneva receives your request.

If you have not completed the 36-month minimum participation period, your request to decrease your coverage is refused.

Please note:

- A new 36-month minimum participation period starts on the date the change request is approved if you choose Health 2.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- Start of equivalent coverage (which, at a minimum, includes drug coverage) through a private group insurance plan

When your request is submitted to us within 30 days following the event: Your request is accepted as of the date of the event.

When your request is submitted to us more than 30 days following the event: Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva received your request.

Please note

- The exemption is accepted even if the 36-month minimum participation period (applicable to Health 2 and Health 3) is not over.

To request this type of change, you must:

Fill out the Request for Change form specifying all of the required information below:

Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- Cessation of equivalent coverage under a private group insurance plan.

When your request is submitted to us within 30 days following the event:

- Your request is accepted as of the date of the event

AND - You can choose the health insurance coverage you want (Health 1, 2 or 3)

When your request is submitted to us more than 30 days following the event:

- Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva received your request

AND - You must continue to participate in Health 2 or Health 3 if your 36-month minimum participation period has not been completed

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible events:

- Marriage / civil union

- Cohabitation for a period of one year

- Birth / adoption / custody of a child

- Termination of spousal coverage

- Separation / divorce

- Death of a dependent

When your request is submitted to us within 30 days following the event: Your request is accepted as of the date of the event.

When your request is submitted to us more than 30 days following the event: Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva received your request.

Please note:

- If you add this benefit, your 36-month minimum participation period starts on the date your request to add is approved.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

WHEN YOUR 36-MONTH MINIMUM PARTICIPATION PERIOD IS OVER

Eligible event:

- No event required

Your request to terminate is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva received your request.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

WHEN YOUR 36-MONTH MINIMUM PARTICIPATION PERIOD IS NOT OVER

Eligible event:

- Start of equivalent coverage

You can terminate your participation during the 36-month minimum participation period if you can establish, to the satisfaction of SSQ, that you are now eligible for another group insurance plan that includes a dental care insurance benefit.

In such case, your request would be approved as of the first day of the premium payment period that coincides with or follows the date SSQ received your request.

Please note:

- If you want to obtain dental care coverage in the future, a new 36-month minimum participation period will start on the benefit’s new effective date.

To request this type of change, you must contact Beneva at 1 877 651-8181.

Eligible event:

- No event required

Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva accepts your evidence of insurability.

Please note

- If you have long term disability insurance, your option selection will also increase for this benefit.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva receives your request.

Please note:

- If you have long term disability insurance, your option selection will also decrease for this benefit.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva accepts your evidence of insurability.

Please note:

- Your option selection for this benefit will be the same as for short term disability insurance.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

Your request is accepted as of the first day of the premium payment period that coincides with or follows the date SSQ receives your request.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva accepts your evidence of insurability.

Please note:

If you want to subscribe to Participant’s Optional Life Insurance, you must first sign up for Option 2 ($50,000) of the Participant’s Basic Life Insurance + Participant’s AD&D Insurance for yourself.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- Marriage/civil union

- Cohabitation for a period of one year

- Birth/adoption/custody of a child

When your request is submitted to us within 30 days following the event: Your request is accepted as of the date of the event.

When your request is submitted to us more than 30 days following the event: Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva accepts your evidence of insurability for your dependents.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva accepts your evidence of insurability for your spouse.

Please note:

If you want to subscribe to Spouse’s Optional Life Insurance, you must first sign up for Option 2 ($50,000) of the Participant’s Basic Life Insurance + Participant’s AD&D Insurance for yourself.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva received your request.

Please note:

- When you request to decrease or terminate one of these benefits, you can participate again, subject to Beneva's approval of evidence of insurability.

- Having Option 2 ($50,000) for your Participant’s Basic Life Insurance + Participant’s AD&D Insurance is a prerequisite for taking out additional life insurance coverage for yourself and your spouse. If your Basic Life Insurance is terminated, these two benefits must be terminated at the same time, if applicable.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

IMPORTANT: If you previously designated an irrevocable beneficiary, you must get that person’s consent to be able to make this change. To do this, use the Request to change irrevocable beneficiary form.

Otherwise, to change a beneficiary who was previously designated as revocable, you can modify it one of the following ways:

- On Client Centre

- Fill out the Request for Change form and send it to us in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

Your request is accepted as of the first day of the premium payment period that coincides with or follows the date Beneva received your request.

Please note:

- To be recognized as a non-smoker, you must declare that you have not smoked any tobacco product, such as cigarettes, cigars or a pipe, or any drugs in the last twelve months.

- Beneva can periodically request confirmation of this status.

- If you do not respond, you will lose the status and no longer receive the lower premium as of the date of our request.

- Any false statement or non-disclosure can nullify your coverage.

To request this type of change, you must:

- Fill out the Request for Change form

- Send us your form in one of the following ways:

Email:

[email protected]

Fax:

1 866 333-7503

Mail:

Beneva

2525, boulevard Laurier

C.P. 10500, succ. Ste-Foy

Québec QC G1V 4H6

Eligible event:

- No event required

Your request will be processed as soon as possible once Beneva receives it.

There are several ways to make this change:

On Client Centre

By email:

[email protected]

By fax:

1 866 333-7503

By phone:

1 877 651-8181

There are several ways to make this type of change:

On Client Centre

By email:

[email protected]

By fax:

1 866 333-7503

You can make this change by:

Email:

[email protected]

Fax:

1 866 333-7503

Discover our app!

Your insurance on the go.

Application mobile disponible sur l'Apple App Store Application mobile disponible sur le Google Play Store